Buy, Lease, or Loan: Financing Your Solar System Has Never Been Easier

Solar panels are an asset to your home that can increase its value, save you money, and increase your energy independence. For many homeowners, there are two important factors to consider: the cost of entry and the ease of installation. After all, time is money, and if you’re already spending a hefty sum on acquiring your equipment, the added cost and time spent installing it can be problematic. We address the latter by selling only DIY solar kits, for which there is no cost of installation, and the job can be done over a weekend. For the former, we look at the options you have for solar power financing. There are also numerous incentives, such as the 30% federal tax credit, and state rebates which can drastically lower your cost for going solar in the long run.

The incentives begin: federal, state, and local

Since 2006, there has been a federal tax credit that underwrites some of the costs of a solar purchase and installation.

The government didn’t have a lot of luck with the original limit of $2,000, so the plan was changed to cover 30% of the total cost of the solar purchase and installation with no upper limit.

Soon, state governments got involved, offering state-sponsored rebates, subsidies, and grants. Eventually local administrations joined in as well and local utilities agreed to buy excess energy that was fed back into the grid, often at twice the going rate that they were charging for electricity.

Why? Because by using a certain percentage of renewable energy, they were granted carbon credits which they could use to offset the pollution they were creating elsewhere.

Both of these programs combined can save you 30-50%, anywhere from $3,000 – $10,000 in the long run, but they’re usually applied after you’ve purchased – which means you still need money up front to actually buy your equipment. Enter your financing options.

Buy, Loan, or Lease?

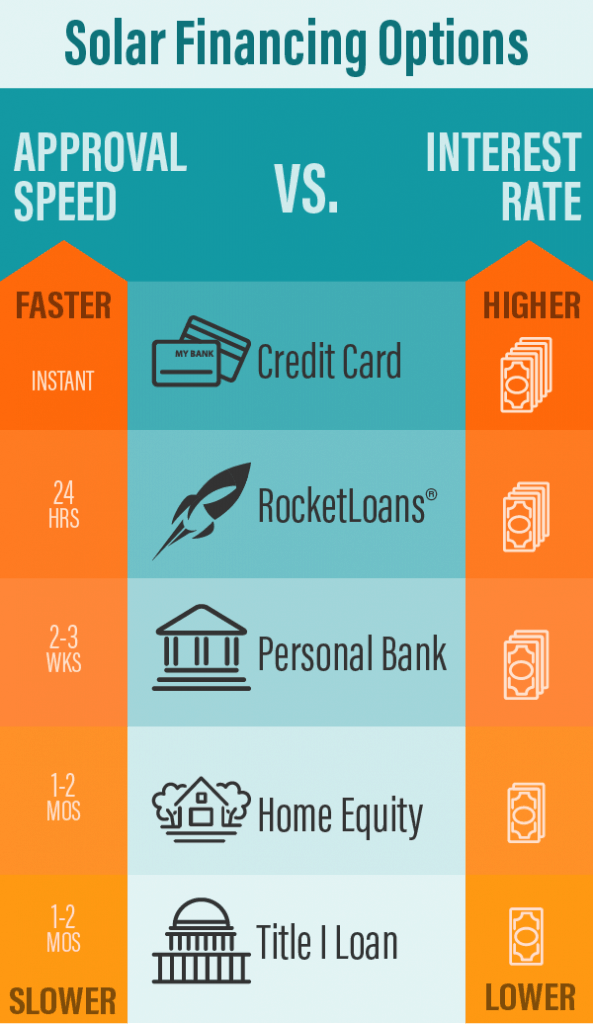

What if I can’t afford to buy a solar system outright? Can I finance it? Some of our customers have enough in savings to purchase a system in cash, which is what we usually recommend (debt can be dangerous!). However, for those who want to take advantage of the Federal Tax Rebate before it sunsets in 2021, there are other options to help with affordability, such as:

- Starting with a smaller system, such as our expandable Enphase solar starter kits (starting from just $1000), and adding more panels later. These have the additional upside of being able to squeeze every last watt out of individual panels under different shading conditions.

- If you’re in California, see if you qualify for the HERO program, financing specifically designed to help homeowners immediately afford renewable energy upgrades to their homes. Annual payments are tacked on to property taxes and the interest may be tax-deductible. For other states, check to see if there is a similar PACE (Property-Assessed Clean Energy) program near you.

- Consider a home equity loan with a local bank or credit union, especially those who participate in the federal PowerSaver loans program (see map of PowerSaver lenders).

- There are more ideas on our Financing Solar page.

If financing your solar system is the only way you can afford one, however, there are financing options available to help alleviate some of the costs. There’s a lot to consider with financing: you’re probably not buying solar purely for ROI, but getting a return on your investment is certainly one of the more enticing factors. Take into consideration how much you’re going to spend buying the solar system, how much you’re going to get back from federal and state incentives, and how long the system is going to take to pay for itself by offsetting your utility bill costs over the years, and you’ve got a good idea of what to expect. Let’s take a look at the three forms of financing, and their various benefits and drawbacks.

Buy:

- If you buy it, you own it.

- There is a fixed, predictable period of time over which it will pay for itself (The “payback period” of 3-6 years, depending on the install), after which it is pure profit (the ROI – Return on Investment).

- It increases the value of your home.

- You get to keep all of the subsidies, grants, and tax credits;

- You get paid for extra power production if your utility allows net metering.

- In most cases you can claim the interest on your loan to purchase the system as a deduction on your taxes, something you cannot do with the solar lease program;

- Systems are very reliable; they hardly ever need maintenance aside from a scheduled inverter replacement a decade or two later. Inverters come with a warranty of 10 years (upgradeable to 20 or 25).

- Upfront cost using your own money, often as a lump sum.

Lease:

- The “zero-down” claims are not entirely true. You may not be giving them cash money, but by signing that power purchase agreement (PPA) or lease, you are giving them your 30% federal tax credit and any eligible state or local incentives. You’re giving them the thousands upon thousands of dollars that should rightfully be in your pocket or your bank account.

- When all the adding up is finally done, you’ll discover that you paid the leasing company more than twice as much as it would have cost you to purchase the system yourself and finance it. With the available incentives it should cost less than $2 per watt (all-in) to install your solar system if you DIY it (like many of our customers do; see our Customer Installs of the Month)

- Leasing is still a commitment, your panels and systems are installed on the home, but can be repossessed and uninstalled if you fall behind on payments.

- Leasing IS however a great option if you’re more concerned about offsetting your power bill and using renewable energy sources instead.

- If you lease a solar system, you are not responsible for the maintenance, upkeep, and operation of it – that falls under the responsibility of the lenders, giving you some added peace of mind, especially if your solar system is on a vacation home or summer getaway.

Loan:

- FHA PowerSaver Loans are available to qualified applicants in many states. These loans help cover the cost of solar installation (among other green energy improvements) and come with a reasonable interest rate.

- With a loan, you’re paying back both the solar system’s costs and anything you owe on your mortgage, property taxes, etc, making any ROI or utility bill offset negligible until the loan is paid.

- Loans can often be paid off in 10 to 20 years, which means you may be paying them off for the entire life of the solar system – by the time your loan is paid off, you may need to replace vital components to keep your solar system functioning.

- A loan is, however, a “quick fix” solution for funding your solar system. Assuming you have the credit to qualify for one, this can be a desirable solution at the cost of a delayed return on your investment.

The Takeaway

Leasing or getting a loan for solar panels is a great idea… for the lender. It is not a consumer-friendly business model. In our recovering economy, loans and solar leases no longer make sense. Those two methods actually represent the most expensive ways for consumers to use solar energy. They were designed for investors to take advantage of a market in recession, not to help homeowners install solar.

Even more insidious is the escalator payment scheme, which allows leasing companies to increase your payment rate by 3% per year for 20 years. By year 20 you’re paying more than 175% of what you paid in year one.

By contrast, buying your panels outright saves you more and more money every year you own it. Even if you have to finance it, with a low enough interest rate there is still a good potential for positive payback.